The Financing Challenges of Structural Transformations in Africa in the Post-Covid-19 Period: An Opportunity to Rethink the Financial Resilience of the Continent

Los retos financieros de las transformaciones estructurales en África en el periodo posCovid-19: una oportunidad para repensar la resiliencia financiera del continente

Mama Hamimida

https://orcid.org/0009-0008-0401-4668

Hassan II University of Casablanca - Morocco

Fecha de envío: 27de junio de 2023. Fecha de dictamen: 6 de noviembre de 2023. Fecha de aceptación: 4 de diciembre de 2023.

Abstract

The decline in economic activity and public revenues during the health crisis continues to burden the budgets of African countries. These financial difficulties are due, on the one hand, to the increase in healthcare expenses and, on the other hand, to the support provided to households and businesses during the lockdown period. This situation limits the actions of governments in pursuing structural transformations.

External resources have declined, with net capital flows to low-income and lower-middle-income countries plummeting. The increase in interest rates in developed countries could push heavily indebted nations into a debt crisis. The situation is further exacerbated by the decrease in foreign currency revenues.

The objective of this article is to outline the main causes of the lack of financing in Africa, which hinders the continuation of structural transformations and the achievement of the desired level of development. At the same time, the article highlights the opportunities for development and better integration into the global economy that arise from this crisis. This will necessarily involve the implementation of innovative and resilient financing systems.

Resumen

El descenso de la actividad económica y de los ingresos públicos durante el periodo de la crisis sanitaria sigue afectando los presupuestos de los países africanos. Estas dificultades financieras se deben, por una parte, al aumento de los gastos sanitarios y, por otra, al apoyo prestado a hogares y empresas durante el periodo de confinamiento. Esta situación limita la acción de los gobiernos en la prosecución de transformaciones estructurales. Los recursos provenientes de financiamiento externo han disminuido, con una caída en picada de los flujos netos de capital hacia los países de renta baja y media-baja. El aumento de los tipos de interés en los países desarrollados podría empujar a las naciones muy endeudadas a una crisis de deuda. La situación se agrava aún más por la disminución de los ingresos en divisas. El objetivo del artículo es esbozar las principales causas de la falta de financiación en África, la cual obstaculiza la continuación de las transformaciones estructurales y la consecución del nivel de desarrollo deseado. Al mismo tiempo, destaca las oportunidades de desarrollo y de mejor integración en la economía mundial que se derivan de esta crisis. Esto necesariamente requerirá la puesta en marcha de sistemas de financiación innovadores y resilientes.

Keywords: post-Covid-19 structural transformations; resilient financing systems; sustainable and inclusive development.

Palabras clave: transformaciones estructurales posCovid-19; sistemas de financiación resilientes; desarrollo sostenible e inclusivo.

Introduction

The decline in economic activity during the health crisis and the resulting decrease in public revenues weigh heavily on the budgets of African countries. The crisis has also led to additional expenses in the healthcare sector and to support households and businesses.

In terms of external resources, the financing deficits for the Sustainable Development Goals for 2030 are expected to worsen (UNCTAD, 2022a). Net capital flows to African countries have decreased. The increase in interest rates in developed countries could also have severe repercussions on heavily indebted developing countries (UNCTAD, 2022b y 2022c). The situation is further exacerbated by the decrease in foreign currency revenues, due to declining exports and the slowdown in the tourism sector.

The article will address a dual issue, firstly enumerating the financing difficulties of structural transformations in post-Covid Africa, and secondly demonstrating how the continent must seize the opportunities, some of which are generated by the same crisis, to better integrate into the global economy. Innovative and resilient financing systems are necessary in order to shield Africa from external constraints and pressures, improve public resources, and attract private capital.

The article will be structured around three main points. Firstly, we will address the internal financial difficulties of pursuing structural transformations in Africa in relation to the deficits in state budgets, the decline in foreign capital inflows to Africa, the decrease in foreign exchange reserves, and the impact of rising interest rates on debt. In the light of this diagnosis, where the main characteristics of the financing systems of African states will be revealed, their weaknesses in the face of the needs of economic growth and development, and their fragilities in the face of external shocks, a theoretical analysis will be presented. The latter will raise the debate on the relevance of the different sources of financing of the economies of the countries, whatever their level of development and their level of income, and will shed light on what is best for the economies of African states. Secondly, we will explore the constraints and/or opportunities that arise for Africa at the international level. Finally, we will emphasize the imperative of establishing resilient and innovative financing systems.

Difficulties at the national level

State Budgets. Just before the crisis, there were decreases in budget deficits from 5.9% of gross domestic product (GDP) in 2017 to 4.8% in 2019 (BAD, 2020a)[1]. Moreover, the global health crisis that paralyzed economies worldwide took a toll on the budgets of African states, pushing them back into deficits due to healthcare expenses and support measures for the population and economic activity. The most significant percentage increase was observed in North Africa, where public spending rose from 42% to 54% during the Covid-19 period. This lack of internal resources persists even after the crisis and limits the actions of governments in pursuing structural transformations.

The high volatility of exchange rates has led to a decline in foreign exchange reserves and prolonged depreciation pressure on most African currencies (CEA, 2021a). This widespread currency depreciation has increased debt service costs, further exacerbating the budget burden. The economic costs associated with travel, trade, and links with financial markets are likely to be significant, as are the direct and indirect spillover effects, further reducing the budgetary leeway of countries that already struggle to finance activities aimed at achieving the Sustainable Development Goals and the goals of the Agenda 2063 (CEA, 2021b).

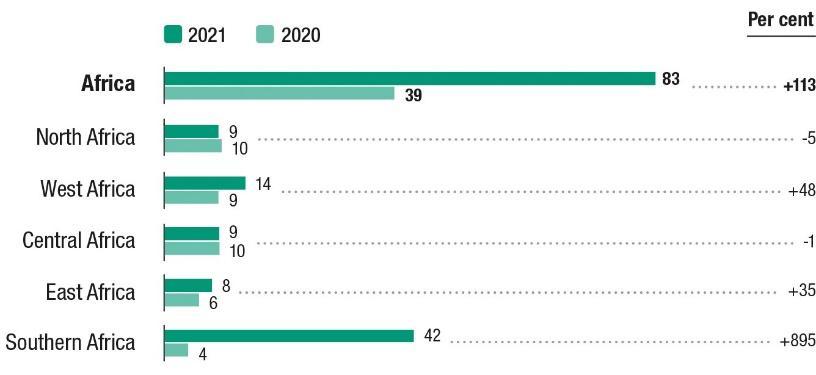

The Decline in Net Capital Flows to Africa. Net capital flows to Africa have declined, exacerbating the financing deficits of the Sustainable Development Goals by 2030. Net capital flows to low-income and lower-middle-income countries have dropped by 85% and 75%, respectively (UNCTAD, 2022a). Despite the improved profitability of foreign investments by multinational corporations in 2021, the value of new projects has decreased compared to the pre-Covid-19 period, except for developing countries where it remained stable. Investment flows to Africa accounted for only 5.2% of global foreign direct investment (FDI) in 2021, up from 4.1% in 2020 (UNCTAD, 2022a), representing a slight increase.

Most African countries experienced a moderate increase in FDI in 2021, but it is important to note that 45% of the total is attributed to an intra-company financial transaction in South Africa (UNCTAD, 2022a). In addition to this, there are regional disparities and variations among countries within the same region. North Africa saw a 5% decrease in FDI flows, with a 52% increase in Morocco and a 12% decline in Egypt. Investment flows to Mozambique increased by 68%, while they plummeted drastically in Zambia (-457 million dollars: a sharp decline compared to -173 million dollars in 2020). It is worth mentioning that investments are generally concentrated in the extractive sectors. In fact, the decline in Zambia is primarily attributed to the sale of a copper mine worth 1.5 billion dollars by the Swiss company Glencore to the state-owned company ZCCM Investments Holdings (UNCTAD, 2022a).

Figure 1. FDI flows to the African continent and sub-regions, 2020-2021 (billions of dollars)

Source: UNCTAD (2022d)

The restrictions on mobility in Africa and prolonged lockdowns have had a significant impact on FDI. Additionally, the closure of external borders has disrupted ongoing projects due to the inability of expatriate workers to return to the continent and carry out their work. Local businesses have also been affected due to the decline in demand resulting from the lockdowns and decreased income. African companies were operating at less than half of their capacity, with micro, small and medium sized enterprises being the hardest hit (CEA, 2020a).

In addition to the issue of real investments, there have been massive withdrawals of portfolio investments, leading to currency depreciation in various countries across the continent. This, in turn, poses a risk for investors and reduces FDI. A volatile currency is not reassuring for ensuring the profitability of investments.

The privatization plans of some countries, which represented sources of capital, have been put on hold due to the Covid-19 crisis. For example, Ethiopia had initiated a bidding process for the sale of a 40% stake in the state-owned enterprise Ethio Telecom to private investors as part of a comprehensive reform program in 2019. However, the project was postponed due to changes in the global economic situation.

The recovery of FDI on the continent appears to be weak, as evidenced by the low level of new projects, including a decrease in all main components of FDI, such as reinvested earnings, infrastructure projects, mergers and acquisitions. However, investments in renewable energies have nearly doubled compared to 2011. Morocco is at the forefront of supplying wind and solar energy, particularly to the United Kingdom.

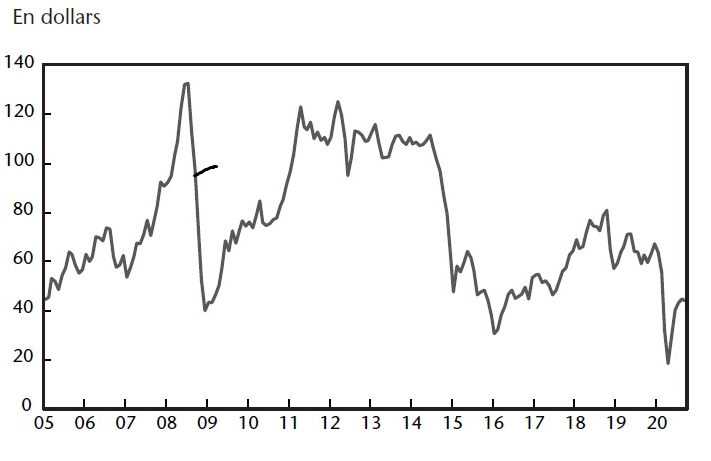

Decline in Foreign Exchange Earnings. In the case of commodity exports, the global economic recession caused by the decrease in demand and supply during the pandemic dealt with a severe blow to the oil market in the spring of 2020. This was manifested by a collapse in demand, an overproduction crisis, and depleted storage capacity. As a result, investors who did not have physical storage capacity had to liquidate their positions. This phenomenon was further amplified by the development of an exchange-traded fund (ETF) based on the West Texas Intermediate (WTI) crude oil[2]. The price of oil plummeted to as low as $20 per barrel, compared to over $100 per barrel between 2011 and 2013 (Fig. 2). A similar but less severe drop had already occurred in 2016. While the negative supply shock is primarily linked to a reduction in workforce due to the spread of the virus and lockdown measures, the negative demand shock is attributed to disruptions in production and global value chains, which have reduced the demand for energy products. The Covid-19 pandemic led to a 9% decline in global consumption, reaching an average of 92.2 million barrels per day (mb/d), marking the sharpest decline since 1980 (Augé, 2021).

Figure 2. Evolution of the price of a barrel of Brent oil

Source: Heyer y Hubert (2020)

Studies on the transmission channels of the oil price decline to consumer and producer prices show that the effects are highly detrimental to oil-producing countries. In Africa, countries such as Nigeria[3], Angola[4], and Algeria[5], already weakened by the 2016 recession, have revised down their growth rates and adjusted their public finances through corrective plans. For other countries like Egypt, the Democratic Republic of Congo, and Gabon, the oil price drop has deteriorated the terms of trade for commodity products and reduced export revenues. The double deficit is widening, adding to the burden of debt. The volume of oil investments worldwide could decrease due to constraints from green finance and the new strategies of major oil companies (Augé, 2021). These majors will be replaced by smaller companies with lower cost structures. This applies to countries such as Nigeria, Angola, Equatorial Guinea, Gabon, and the Republic of Congo. The withdrawal of these majors and the consequent reduction in large investments in the sector will have an impact on production volume.

These circumstances urge these countries to revise their model and reduce their dependence on oil by diversifying their economies and continuing the process of structural transformation. This process has already faced challenges in oil-producing countries, driven by fluctuating production and prices, and marked by strong resilience to recessions. Meanwhile, from a socio-economic standpoint, populations suffer from difficulties in accessing public services, the effects of climate change, and security issues.

The need for restructuring is further amplified by environmental constraints. These countries face increased vulnerabilities due to environmental constraints, as the exploitation of their reserves is characterized by declining production and rising costs. This is particularly true for Gabon, Congo, Equatorial Guinea, Côte d'Ivoire, Angola, and the DRC. To remain significant oil producers by 2030 and maximize the economic benefits of these resources, they will be compelled to undertake profound fiscal and governance reforms (Augé, 2021).

As for the decline in the tourism sector, in 2020, Africa experienced a 70% decline in tourist arrivals, according to the latest report by the World Tourism Organization (UNWTO). This figure is slightly lower than the global average of 74% (UNWTO, 2022), but it has had significant implications for certain countries. For instance, in Kenya, where tourism accounts for 9% of GDP and 10% of employment (Xinhua, 2021), the impact has been severe. Similarly, in the Seychelles, where tourism contributes to 30% of GDP (World Bank, 2020), the decline has been significant. Another example is Mauritius, a popular destination for South Africans, which witnessed a 77% drop in arrivals. Tourism constitutes 24% of the country's GDP and employs 22% of the workforce (BAD, 2021b).

The tourism sector contributed with 7% to the GDP of the continent in 2019. Apart from the revenue it generates, tourism in Africa fuels economic transformation, accelerates reforms, triggers improvements in infrastructure, and strengthens the position of women and minorities throughout Africa (World Bank, 2013).

The tourism sector faces many obstacles to its expansion, particularly in Sub-Saharan Africa, where land ownership, land availability, and land rights transfer still pose problems and do not receive sufficient attention from.

Tourism in Africa has the potential to be a significant source of wealth, but it is an area that remains largely untapped by governments. They need to integrate it as a lever in their development plans because it generates revenue and creates jobs, both for skilled individuals and marginalized populations such as women and youth. Governments must take measures to enhance the attractiveness of their countries, liberalize air transport, provide training for high-quality service personnel, ensure currency convertibility, and most importantly, ensure security within their territories.

Rising Interest Rates and Impact on Debt. The public debt service of sub-Saharan African countries has more than tripled between 2010 and 2019, with the debt service as a percentage of public revenues increasing, indicating significant vulnerability in certain countries, for example, in Nigeria, where it reached nearly 85.5% in 2021 and is projected to reach 139% in 2026 (Hooper, Le Clainche y Seitz, 2022). The decline in GDP and revenues due to the decrease in supply and demand during the health crisis, the drop in commodity exports due to the global economic slowdown, and the decrease in international transfers during this same period have exacerbated this vulnerability, leading several countries on the continent to be classified as heavily indebted. For some oil-exporting and/or tourism-dependent countries, the high exchange rate volatility has depleted their foreign exchange reserves, thus weakening their capacity to meet foreign currency-denominated obligations. The GDP of oil-exporting countries is estimated to have contracted by 1.5% in 2020, with Algeria, Angola, Equatorial Guinea, Libya, and Nigeria being the most affected (BAD, 2021a). Furthermore, exchange rate volatility remained high in tourism-dependent economies (such as Mauritius and Seychelles) and resource-intensive economies, eroding foreign exchange reserves and exerting sustained downward pressure on most African currencies.

The rise in interest rates in developed countries to curb inflation could also have severe repercussions in heavily indebted developing countries, particularly in Africa, which lacks budgetary and financial resilience. As inflation increases, interest rates rise. These high debt costs, combined with declining revenues, further weaken African countries.

The problem is that this situation is not new, and Africa fails to learn from its experiences. The financing needs expressed by Africa during independence to spur economic growth sharpened the appetite of international financial institutions and western lending countries. Between 1970 and 1987, Africa's total external debt increased from 8 billion to 174 billion US dollars, and the ratio of external debt to GDP (total external debt outstanding as a percentage of GDP) rose from 16% to 70% (Ambassade de la Republique Populaire de Chine en Republique Francaise, 2022).

According to the 2022 edition of the World Bank's International Debt Statistics, multilateral financial institutions and commercial creditors hold 28.8% and 41.8% of Africa's external debt, respectively, accounting for nearly three-quarters of the total debt. In addition to that, China holds 17% of Africa's external debt. The increase in interest rates raised the cost of debt servicing and led African countries into a debt crisis in the late 1980s. Apart from the financial impact, indebtedness has harmed Africa in terms of attractiveness for FDI and limited its access to international market financing. However, differences exist among African countries. In fact, some countries can serve as models son they have successfully managed their debt through highly effective strategies. A return to the theoretical postulates will further clarify the problem of financing development in Africa.

Brief Analysis of the Theoretical Postulates Underlying the Financing Problem. In traditional analyses, savings are at the center of the relationship between the financial system and economic development. This involves its mobilization and allocation to profitable investments thanks to positive real interest rates. This is on the internal level. Externally, when savings are not sufficient for the required investment and/or when imports exceed exports, external resources will then fill the balance of payments deficit. For other analyses, notably Keynesian analysis, it is investment which is at the origin of savings because it causes an increase in consumption which in turn increases investments. The State must intervene by stimulating effective demand.

This interventionist perspective is confronted with the liquidationist perspective developed by Carl Menger, Friedrich Hayek and Roger Garrison, who consider savings essential to growth because they finance investment.

Some authors (Paul Beaudry, Dana Galizia and Franck Portier, 2014) seek to reconcile the Heyekian and Keynesian perspectives on recessions. Severe recessions like the 1970s and the 2008 crisis, were preceded by periods of strong capital accumulation. In his growth model, Solow (1956) states that an increase in the savings rate leads to a temporary increase in the growth rate.

The results of these debates show that there is a long-term correlation between savings and economic growth but the causal relationship has not been verified. Economic developments in East Asia show that it is economic growth that has led to an increase in savings. But then, how can we design an effective financing system for growth and development on the African continent which remains largely dependent on the outside?

Growth is the result of an increase in investment and a fall in the real exchange rate. This confirmation raises the question of external savings and internal savings.

An economic analysis, particularly that emanating from conventional orthodoxy, shows that foreign capital increases the exchange rate and limits investments intended for export. But a competitive exchange rate is necessary. Empirical studies demonstrate this and the rapid growth of Asian countries clearly confirms it. But research in economics is not abundant when it comes to seeing the relationship between exchange rates and economic growth.

Economic history shows us that the domestic market and exports are essential for economic growth and development. These exports must concern products with high added value so that they can be profitable for the country; this requires a prior industrialization phase which would ensure the transfer of work from sectors with low added value to sectors with high added value. External demand favors this process. Countries must have technological capacity and a competitive exchange rate. This is the case for Asian countries, Brazil and Mexico, the latter concentrated on the energy sectors and agricultural export production. And this is one of the major differences with African countries. The latter have not been able to develop their own technology or benefit from technology transfer through FDI.

International Constraints to the Pursuit of Structural Transformations in Africa

Criteria of Structural Transformation Process. Structural transformations require a set of actions, such as the development of high-productivity activities, the growth of manufacturing industries and modern services, the reduction of the agricultural sector's share in employment, managing the rapid expansion of the services sector, reducing dependence on natural resources, increasing the relative contribution of the manufacturing sector to GDP, demographic transition, controlled urbanization, and investment in technology.

This process also involves upgrading within sectors, as production becomes more intensive in terms of skill, technology, and capital. Furthermore, sectoral changes tend to strengthen the dominance of sectors and activities with higher growth potential, in terms of both income elasticity of demand and the presence of increasing returns to scale and technological progress (UNCTAD, 2012).

The economic development of most industrialized and emerging countries has been characterized by an increase in employment in the industrial sector, followed by the services sector, at the expense of the agricultural sector. Productivity gaps between sectors have resulted in income disparities, urbanization differences, and the expansion of the middle class. These structural transformations need to be sustainable, meaning that there should be a relative decoupling between environmental impact and the growth process. They are essential for long-term economic growth and enable a reallocation of sectoral demand towards less resource-intensive uses.

The State of the Process Before and After the Health Crisis. Just before the health crisis, the continent achieved strong growth performance, driven in particular by a gradual increase in investments and net exports at the expense of private consumption. Six of the top ten fastest-growing economies in the world are leading the way: Rwanda, Ethiopia, Côte d'Ivoire, Ghana, Tanzania, and Benin (BAD, 2020a). This followed the situation in 2011-2012 when the African continent was ranked as the second-fastest-growing region in the world, behind East Asia (CEA, 2012). Between 2000 and 2009, 11 African countries achieved a growth rate equal to or higher than 7%. However, the processes of structural transformation have not been inclusive. A true process of economic transformation should address inequalities, unemployment, and the very poor quality of social services. This is fundamental to human development and, consequently, the successful implementation of other aspects of the transformation agenda, such as improving human capital and technological progress, among others.

The African Continental Free Trade Area (AfCFTA) was created with the aim of developing intra-African trade and industry, diversifying exports, strengthening regional value chains, and moving up the global value chains. However, for this zone to fully contribute to the diversification and inclusive transformation of all economies on the continent, African states must develop effective export policies and strategies, identify opportunities for export diversification, industrialization, and supply chain development (UNCTAD, 2022b).

In addition to the shortcomings of the structural transformation process in Africa, the global health crisis has paralyzed economies worldwide and had consequences for African countries in terms of slowing down their structural transformation programs.

Furthermore, the impact of the Russo-Ukrainian conflict on the African economy cannot be ignored. Economic growth in Africa is expected to decline to 3.8% in 2023, compared to 4.1% in 2022, due to weak investments and a decline in exports. This performance is lower than the nearly 7% growth achieved in 2021 (UNCTAD, 202b). As a result, several million additional Africans will fall into extreme poverty in the coming years. They will join the 55 million people already pushed into extreme poverty by the Covid-19 pandemic (UNCTAD, 2022c). The Russo-Ukrainian conflict has hindered the rebound of growth after the health crisis. Economic growth could remain "frozen" at the level of 4.1% in 2023 (BAD, 2020c).

Constraints and/or Opportunities at the International Level. The global health crisis has generated radical changes in global production, characterized by an increased trend towards shortening global value chains and the relocation of industrial activities. Foreign companies are inclined to reassess their investment strategies in order to reduce the distance between production sites, suppliers, and global markets. In this case, China risks losing its status as the world's factory, and Africa can seize this opportunity to become the preferred destination for these multinational corporations.

However, rapid technological progress (digitalization, automation, robotics, the Internet of Things, Industry 4.0, etc.) is impacting all production processes and sectors and requires a parallel development of human capital. Unfortunately, the scarcity of human capital in Africa leads to brain drain, partly due to the lack of industrial development on the continent and partly to the search for rewarding, innovative, and better-paid job opportunities elsewhere. Africa, with its human capital and labor costs, should seize this opportunity to integrate into global value chains with intangible value additions. This is further encouraged by the increasing concentration of value-added services and the growth of the services trade, which present opportunities for developing countries to integrate into the global economy (IRES, 2022). The latest report of the UNCTAD (2022b) calls on African states to diversify their exports and encourage the export of high value-added services in FinTech. In developing countries, exports are growing more strongly in telecommunications and ICT services, financial services, and other business services. On the other hand, in developed countries, there is a concentration of higher value-added services such as financial services. (UNCTAD, 2022b).

The trade in services, which is experiencing rapid and intense growth due to the evolution of the digital economy, is more resilient to economic crises compared to the trade in goods. This presents an opportunity for developing countries to participate in global trade regardless of their level of development or size. Services are major inputs in all productive activities and enable countries to better position themselves in global value chains (Hamimida, à paraitre), thus making African economies more resilient.

Indeed, industrialization is not solely about infrastructure and human capital. In some countries, enormous expenditures have been made to establish industrial zones that have remained empty due to a lack of investment from local businesses, insufficient FDI, limited international and regional cooperation, administrative rigidity, discouraging taxation, and so forth. As for human capital, if African governments are unable to retain it in their home countries through effective industrialization programs (based on production diversification, technology, high value-added production, access to international markets, and the development of intra-regional cooperation, among other factors), it will inevitably serve other industrialized countries in the North.

Africa has experienced two decades of failed industrialization programs. The Decade of Industrial Development in Africa (IDDA 1), launched in 1980, failed due to a lack of financing. IDDA 2, supported by the African Union and the United Nations Industrial Development Organization (UNIDO) in the 2000s, failed due to the decline in commodity prices.

The objectives of IDDA 3 are linked to the African Union's Agenda 2063 for Africa's development and are anchored in the Sustainable Development Goals, particularly SDG 9: “Industry, Innovation, and Infrastructure”. Its implementation takes place in a radically changing context driven by the Covid-19 crisis.

It is encouraging to note that despite the challenges, some African countries have managed to make progress in the manufacturing and agro-industrial sectors (food and beverages, leather, textiles, automotive, and heavy machinery), although diversification is still insufficient. Ghana, for example, has aimed at developing export-oriented Special Economic Zones (SEZs). The Ghanaian industrial sector has recorded an average annual growth rate of over 10% for the past three years, making it a crucial factor in the country's overall growth (UNIDO, 2019). In Uganda, there has been an increase in the industrial sector's contribution from 20% to 30% in 2019, accompanied by improvements in job creation (UNIDO, 2019).

However, Africa remains the least industrialized region, with its contribution to global value-added manufacturing remaining insignificant. In 2018, the most recent year for which data is available, Africa's share was only 10.5%, compared to over 16% in the early 1980s, while it reached over 25% in developing Asian countries in recent years.

The share of intra-African regional trade (17% of exports) is significantly lower than that of Europe (67%) or Asia (60%), but almost half of these exchanges involve manufactured goods, which is much higher than in other regions of the world (UNIDO, 2019).

Indeed, Africa is facing various constraints related to technological advancements, energy transition, and environmental challenges such as drought and decarbonization. However, it also has opportunities that can propel it towards a better position in the global economy. Africa has the potential to become a preferred destination for multinational firms due to its proximity to Europe, its human capital, its labor costs, and the emergence of an African middle class. The African Development Bank defines the middle class as individuals with a purchasing power of $2 to $20 per day. By 2050, this middle class is expected to reach 40% of the population, which is more than one billion people according to the African Development Bank.

Additionally, Africa has considerable untapped potential in terms of renewable energy. The BloombergNEF Report 2023[6], highlights that by 2050, global electricity production will primarily come from wind power (48%), solar power (26%), and other renewable energy sources (7%). Africa, in particular, has evident potential in solar energy, but it only accounts for 1.3% of global solar energy capacity, according to the same report. However, some countries such as Morocco, Egypt, South Africa, and Kenya have made this sector a future industry by developing sources of green electricity, including solar and wind energy. For instance, Morocco has significant potential in green energy, making it one of the world's major energy producers, with high competitiveness, and regulations and institutional provisions that incorporate best international practices (IRES, 2022). This availability of renewable energy, in addition to boosting the economies of certain countries on the continent through FDI, will have a ripple effect by reducing production costs in other sectors of the economy such as textiles, and facilitating the integration of countries into global value chains and global value networks with stronger backing. Through intra-regional cooperation and trade, the entire continent can benefit from this opportunity.

Africa should also integrate into the carbon finance value chain and develop a structured innovation system for clean technologies and green businesses (Sy, 2011). Other sectors can represent potential for Africa, such as the electric vehicle battery industry. With their abundant resources of cobalt and lithium, countries like the Democratic Republic of Congo (DRC), Madagascar, and Morocco can become destinations for Asian battery manufacturers.

The imperative to rethink strategies for achieving and completing structural transformations in Africa after Covid-19 also entails rethinking financing systems.

Resilient and Sustainable Financing Systems

The International Monetary Fund has established the Resilience and Sustainability Trust, enabling African countries to maintain their structural transformations and address climate change and its consequences (such as drought and poverty), as well as potential health crises related to virus outbreaks. In fact, nine out of ten countries most vulnerable to climate change in the world are African (NG-GAIN, 2023). So far, only Rwanda has been able to benefit from this funding.

A resilient economy is indeed important, but there is an even better approach: resilient financing. This approach aims to help Africa break free from dependence on raw materials, debt, and conditionality-based development aid, and achieve its structural transformations. The common position of Africa on the post-2015 development agenda prioritizes domestic resource mobilization as a key source of development financing. Risks associated with climate change, pandemics, external shocks, and others should be taken into account in macro-fiscal frameworks. Structural transformations need to be funded through guaranteed resources. Achieving the Sustainable Development Goals in Africa by 2030 is estimated to require approximately $1.3 trillion per year (CEA, 2020b).The financing needs for infrastructure in Africa range from $130 billion to $170 billion per year until 2025, with an annual financing deficit of $67.6 billion to $107.5 billion (BAD, 2018). Despite its significance, the infrastructure sector does not attract significant private financing, as investors tend to prefer sectors with lower costs, lower risk, and higher returns, such as energy or information and communication technologies.

African governments should develop public-private partnerships that have been successful in many countries for the construction and operation of transportation infrastructure, railways, airports, healthcare centers, and oil and gas production. Such financing models have been effective in countries like India and China.

Africa can also finance its development through national and sub-regional development banks, which can attract private capital, but this requires the development of local and regional capital markets. These markets are important for national banks to provide loans in local currencies and directly finance bond issuance.

Sovereign wealth funds can finance investments by utilizing the accumulated revenues from natural resource exploitation and contributing to the capital of national development banks.

Financing structural transformations through equity funding may be challenging due to the narrow tax base resulting from a weak private sector, low per capita income, a weak industrial sector, and the intensification of the informal sector. However, expanding this tax base requires successful structural transformations, including the presence of a dense industrial fabric, advanced and progressive technologies, companies producing high value-added goods, competitive exports in international markets and a competitive rate of change. Africa is caught in a vicious cycle that can be transformed into a virtuous circle. Modernizing traditional financing channels and mechanisms for private sector financing, both domestically and internationally (provided that interest rates are not abusive), should be a priority.

Strengthening local financing systems and mobilizing domestic savings, along with regional financial integration, are crucial for ensuring inclusive and resilient financing in Africa. Central banks need to unlock unused resources to boost productive investments. Over 1 trillion US dollars of excess reserves have not been effectively utilized to finance Africa's development. The role of central banks should not be limited solely to controlling inflation (often imported), but also to allocating resources towards productive investments and implementing sectoral exchange rates to encourage exports, as is the case in Brazil.

There is also a need for increased transparency in international financing and stronger regulation of financial markets, as well as a revision of debt terms and negotiation conditions to assist heavily indebted countries in their development efforts.

Conclusion

The health crisis has undermined two decades of positive growth and development in Africa. All experts recommend increasing aid and financing to build resilient economies on the continent. African states find themselves facing expenses related to external debt repayment and current account deficits, while also needing to invest in structural transformations to achieve development goals (development programs, achieving the Sustainable Development Goals, promoting green industries, addressing climate change, etc.). International financial institutions have not been of great help or timely enough during the health crisis, even before it occurred. The pandemic further worsened the financial situation of countries on the continent, as they had to allocate significant resources to provide healthcare to the population and support businesses and households during the period of lockdown.

Given the lessons learned from the health crisis and the evolution of the global economy in general (rapid technological progress, shortening of global value chains, environmental constraints, etc.), Africa must not only develop inclusive development strategies that ensure the resilience of its economies and enable it to seize opportunities to integrate into value chains and move up the value ladder, but also strengthen the resilience of its financing. Resilient financing is a lever for reducing poverty and inequality and achieving inclusive and sustainable development.

Bibliographic references

AEC (African Economic Conference). (2021). Financing Africa’s post-Covid-19 development. Cabo Verde, 2-4 December. Available at: https://aec.afdb.org/en/past-aecs/african-economic-conference-2021 [retrieved: May 2023].

AMBASSADE DE LA REPUBLIQUE POPULAIRE DE CHINE EN REPUBLIQUE FRANCAISE. (2022). Encore des questions à clarifier au sujet de la dette africaine. Disponible ici: http://fr.china-embassy.gov.cn/fra/zfzj/202212/t20221216_10991331.htm [dernière consultation: mai 2023].

AUGE, Benjamin. (2021). Conséquences économiques et politiques de la chute de la production pétrolière en Afrique subsaharienne à l’horizon 2030. Paris: Ifri.

BAD (Banque Africaine de Développement). (2018). Perspectives économiques en Afrique 2018.

BAD (Banque Africaine de Développement). (2020a). Perspectives économiques africaines. Former la main d’œuvre africaine de demain.

BAD (Banque Africaine de Développement). (2020b). Perspectives économiques africaines. Soutenir la résilience climatique et une transition énergétique juste en Afrique.

BAD (Banque Africaine de Développement). (2021a). La vulnérabilité de l’Afrique à la dette et sa reprise après la pandémie de coronavirus. Note d’orientation. 2021. Disponible ici: https://repository.uneca.org/bitstream/handle/10855/48299/b12007870.pdf [dernière consultation: mai 2023].

BAD (Banque Africaine de Développement). (2021b). Perspectives économiques à l'île Maurice. Disponible ici: https://www.afdb.org/fr/countries/southern-africa/mauritius/mauritius-economic- [dernière consultation: mai 2023].

BEAUDRY, Paul; GALIZIA, Dana; and PORTIER, Franck. (2014). Reconciling Hayek's and Keynes Views of Recessions. Cambridge, MA: National Bureau of Economic Research.

CEA (Commission Économique pour l’Afrique - Nations Unies). (2012) Rapport Economique sur l'Afrique 2012 : Libérer le Potentiel de l'Afrique en Tant Que Pôle de Croissance Mondiale.

CEA (Commission Économique pour l’Afrique - Nations Unies). (2020a). Le Covid-19 en Afrique : Sauver des vies et l’économie. Disponible ici: https://www.uneca.org/publications/COVID–19-africa-protecting-lives-and-economies [dernière consultation: mai 2023].

CEA (Commission Économique pour l’Afrique - Nations Unies). (2020b). Financement innovant pour le développement des entreprises en Afrique. Rapport économique sur l’Afrique 2020.

CEA (Commission Économique pour l’Afrique - Nations Unies). (2021a). La vulnérabilité de l’Afrique à la dette et sa reprise après la pandémie de coronavirus. Note d’orientation. 2021. Disponible ici: https://repository.uneca.org/bitstream/handle/10855/48299/b12007870.pdf [dernière consultation: mai 2023].

CEA (Commission Économique pour l’Afrique - Nations Unies). (2021b). L’impact macroéconomique de Covid-19 sur l’Afrique. Données d’un modèle macroéconométrique agrégé pour l’ensemble de l’Afrique.

HAMIMIDA, Mama. (à paraitre). “La migration des compétences, un frein à une meilleure insertion des pays d’Afrique dans l’économie mondiale”.

HEYER, Eric and HUBERT, Paul. (2020). “The impact on French households and business of the fall in the price of oil due to the Covid-19 crisis”. Revue de l'OFCE, 168-4, 137-162. Disponible ici: https://www.cairn-int.info/article-E_REOF_168_0137--the-impact-on-french-households-and.htm [dernière consultation: mai 2023].

HOOPER, Emma; LE CLAINCHE, Valentine; et SEITZ, Clément. (2022). L’endettement de l’Afrique subsaharienne, Direction générale du Trésor – République Française, janvier 2022. WATHI Think Tank. Disponible ici: https://www.wathi.org/lendettement-de-lafrique-subsaharienne-direction-generale-du-tresor-janvier-2022/ [dernière consultation: mai 2023].

IRES (Institut Royale des Etudes Stratégiques). (2022). L’avenir des métiers mondiaux au Maroc. Rabat: IRES.

ND-GAIN (Notre Dame Global Adaptation Initiative). (2023). Country Index Technical Report. Available at: https://gain.nd.edu/our-work/country-index/ [retrieved: May 2023].

SOLOW, Robert. (1956). “A Contribution to the Theory of Economic Growth”. The Quarterly Journal of Economics, 70-1, 65-94.

SY, Sams. (2011). Financement du développement résilient au climat en Afrique. Evaluation prospective, cadre stratégique et plan d’action. Harare: Fondation pour le Renforcement des Capacités en Afrique. Disponible ici: https://elibrary.acbfpact.org/acbf/collect/acbf/index/assoc/HASH01c2/d0ee8254/bf7b99ff/3a40.dir/file%20096.pdf [dernière consultation: mai 2023].

UNCTAD (United Nations Conference on Trade and Development). (2012). Economic development in Africa. Structural transformation and sustainable development in Africa. Report.

UNCTAD (United Nations Conference on Trade and Development). (2022a). Financing for development: Mobilizing resources financial support for sustainable development after the Covid-19 pandemic. Geneva: Author.

UNCTAD (United Nations Conference on Trade and Development). (2022b). Rethinking the Foundations of Export Diversification in Africa. The Catalytic Role of Business and Financial Services. Economic Development in Africa. Report 2022. Available at: https://unctad.org/system/files/official-document/aldcafrica2022_en.pdf [retrieved: May 2023].

UNCTAD (United Nations Conference on Trade and Development). (2022c). Trade and Development Report. 2022. Development prospects in a fractured world: Global disorder and regional responses. Available at: https://unctad.org/system/files/official-document/tdr2022_en.pdf [retrieved: May 2023].

UNCTAD (United Nations Conference on trade and development). (2022d). World Investment Report 2022. International tax reforms and sustainable investment. Available at: https://unctad.org/publication/world-investment-report-2022 [retrieved: May 2023].

UNIDO (United Nations Industrial Development Organization). (2019). Troisième décennie de développement industriel de l’Afrique – IDDA III (2016-2025). Quelles chances de succès? Disponible ici: https://www.unido.org/news/troisime-dcennie-du-dveloppement-industriel-de-lafrique-quelles-chances-de-succs [dernière consultation: mai 2023].

UNWTO (United Nations World Tourism Organization). (2022). Data of the Global survey among its UNWTO Panel of Tourism Experts on the impact of Covid-19 on tourism and the expected time of recovery. Madrid. Author.

WORLD BANK. (2013). Africa Tourism Report 2013: More Tourists Visit Africa Each Year, Boosting Economic Growth and Making the Continent Competitive with Other Regions. Available at: https://www.worldbank.org/en/region/afr/publication/africa-tourism-report-2013 [retrieved: May 2023].

WORLD BANK. (2020). The World Bank in Seychelles. Available at: https://www.worldbank.org/en/country/seychelles/overview [retrieved: May 2023].

XINHUA. (2021). “Kenya's tourist arrivals hit rock bottom in 2020 amid pandemic”. Xinhuanet, February 19. Available at: http://www.xinhuanet.com/english/africa/2021-02/19/c_139750926.htm [retrieved: May 2023].

[1]Notes

In contrast, public debt and publicly guaranteed debt were increasing in most African economies, with the median public debt-to-GDP ratio exceeding 56% in 2018, up from 38% ten years earlier.

[2] West Texas Intermediate (WTI) is a benchmark value in the American oil market. Brent, on the other hand, is a benchmark value for a much broader market.

[3] Nigeria is the largest hydrocarbon producer in Africa. Oil production represents over half of its public revenues.

[4] Hydrocarbon exports account for just over 70% of Angola's revenues.

[5] The country is the third-largest producer on the continent. Oil and gas exports account for slightly over 50% of the state's revenue

[6] The BloombergNEF 2023 report was published on the occasion of COP27.